|

|

|

|

|

|

|

The need for the Fifth Market was a direct result of NASD rules changes to SOES (the Small Order Execution System). SOES was created in 1984 to automatically execute small orders in Nasdaq stocks against the best available quotations. |

|

|

|

|

|

|

|

|

After the crash in October 1987, when the small investor was unable to exit his plummeting shares at any price, the regulators strengthened the requirements for market makers in SOES. The intention was for the market makers to be a ready supply of liquidity for the market at all times. |

|

|

|

|

|

|

|

|

Several years later, Harvey Houtkin and a small group of enterprising traders realized the execution advantages of trading against SOES market makers who were slow in adjusting their prices, and the "SOES bandits" were born. Executions against SOES grew rapidly. |

|

|

|

|

|

|

|

|

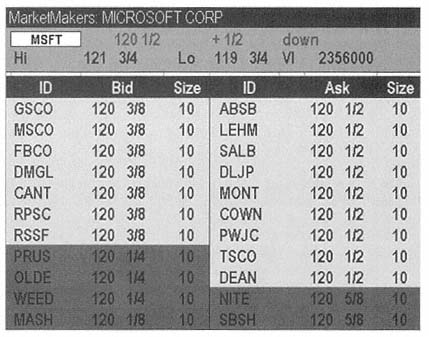

By 1995, market makers on SOES were required to fill two orders for 1,000 shares each at their posted price. A typical level II screen in 1995 for Microsoft (MSFT) might have looked like the one in Figure 1.2. |

|

|

|

|

|

|

|

|

Figure 1.2

1995 Level II Screen |

|

|

|

|

|